What dividends are

Dividends are payments made by a corporation to its shareholders, typically representing a portion of the company's profits. Companies may distribute dividends as cash, or in the form of additional shares. Dividends are often expressed as a fixed amount per share, known as the dividend per share (DPS), or as a percentage of the share price, referred to as the dividend yield.

Regular dividend payments signal a company’s financial health and commitment to returning value to its shareholders. However, not all companies pay dividends; some reinvest their earnings to promote growth or pay down debt. The decision to issue dividends is influenced by various factors, including the company’s earnings, cash flow, and investment opportunities.

Investors often seek dividend-paying stocks for their potential to provide steady income and the prospect of long-term capital appreciation. Ultimately, dividends play a crucial role in attracting and retaining investors within the equity markets.

How dividends are distributed

A dividend is distributed as a specific amount per share, with shareholders receiving payments proportional to their ownership. While dividends can offer a relatively stable source of income and enhance shareholder sentiment, they are not guaranteed to persist.

For a joint-stock company, paying dividends is not considered an expense; instead, it represents the allocation of after-tax profits to shareholders. Retained earnings—profits that are not distributed as dividends—appear in the shareholders' equity section of the company's balance sheet, alongside issued share capital.

Public companies typically issue dividends on a regular schedule, but may cancel scheduled payments or declare unscheduled ones at any time. These unscheduled payments are often referred to as special dividends to differentiate them from regular ones. They may be issued concurrently with regular dividends but for a one-time higher amount. In contrast, cooperatives distribute dividends based on member activity, leading to their dividends often being viewed as a pre-tax expense.

Dividend payout scenarios

Dividends can be paid out in various situations, often reflecting a company's financial strategy. Here are some common examples:

Profit distribution

When a company earns a profit, it may choose to distribute a portion of that profit to shareholders as dividends. This is common for established companies with stable earnings.

Quarterly earnings reports

Many companies announce dividends in conjunction with their quarterly earnings. If they report strong financial results, they may declare dividends to reward shareholders.

Special dividends

Occasionally, companies may issue special one-time dividends, often when they have excess cash due to extraordinary profits or asset sales. This can be a way to distribute surplus funds.

Consistent dividend policies

Some companies follow a consistent policy of paying dividends annually or semi-annually, regardless of fluctuations in earnings. This builds shareholder confidence and attracts income-focused investors.

Tax considerations

Companies may also declare dividends towards the end of the fiscal year for tax planning reasons, providing shareholders with income that can be taxed at favorable rates.

Mergers or acquisitions

In the context of mergers, acquired companies may distribute dividends as part of the acquisition process, especially if the acquiring company seeks to restructure its finances.

Each of these scenarios reflects a company's strategic decisions regarding capital allocation and shareholder value.

How dividend frequency is determined

Dividend frequency refers to how often a company pays dividends to its shareholders. This frequency can vary widely among companies and is determined by several factors:

Company policy

A firm’s board of directors typically establishes a dividend policy that outlines its approach to dividends. This policy may include how often dividends are paid (e.g., quarterly, semi-annually, or annually) based on the company’s strategy and growth objectives.

Cash flow availability

Companies assess their cash flow and ensure they have enough liquidity to cover regular dividend payments. If a company has strong, consistent cash flow, it may opt for more frequent dividend payments.

Earnings stability

Companies with stable and predictable earnings are more likely to pay dividends regularly. In contrast, firms with fluctuating or uncertain earnings might prefer to pay dividends less frequently or not at all.

Investor expectations

Companies may consider investor preferences when determining dividend frequency. For example, income-focused investors often prefer quarterly dividends, which provide a steady income stream.

Market practices

Industry norms can also influence dividend frequency. For example, many established, mature companies in certain sectors (like utilities) typically pay dividends quarterly, while growth-oriented technology firms may opt for annual dividends or forgo them altogether.

Ultimately, the decision regarding dividend frequency is a strategic choice that reflects a company's financial health, growth plans, and the needs and preferences of its investors.

How dividends work for investors

For investors, dividends provide a reliable income stream, making dividend-paying stocks particularly attractive for income-focused investors and retirees. Investors often assess the dividend yield, which expresses dividends as a percentage of the stock’s price, to evaluate the return on their investment.

Companies generally announce their dividends on a quarterly basis. They also establish a record date to determine which shareholders are eligible to receive the payout. It's important for investors to understand the payout ratio, which indicates the percentage of earnings paid out as dividends.

A very high payout ratio might raise concerns about sustainability. While dividends are a sign of financial health, investors should also consider the company's growth potential. Some firms reinvest earnings for expansion rather than distributing them. Overall, dividends can enhance total investment returns by providing both income and potential appreciation in stock value.

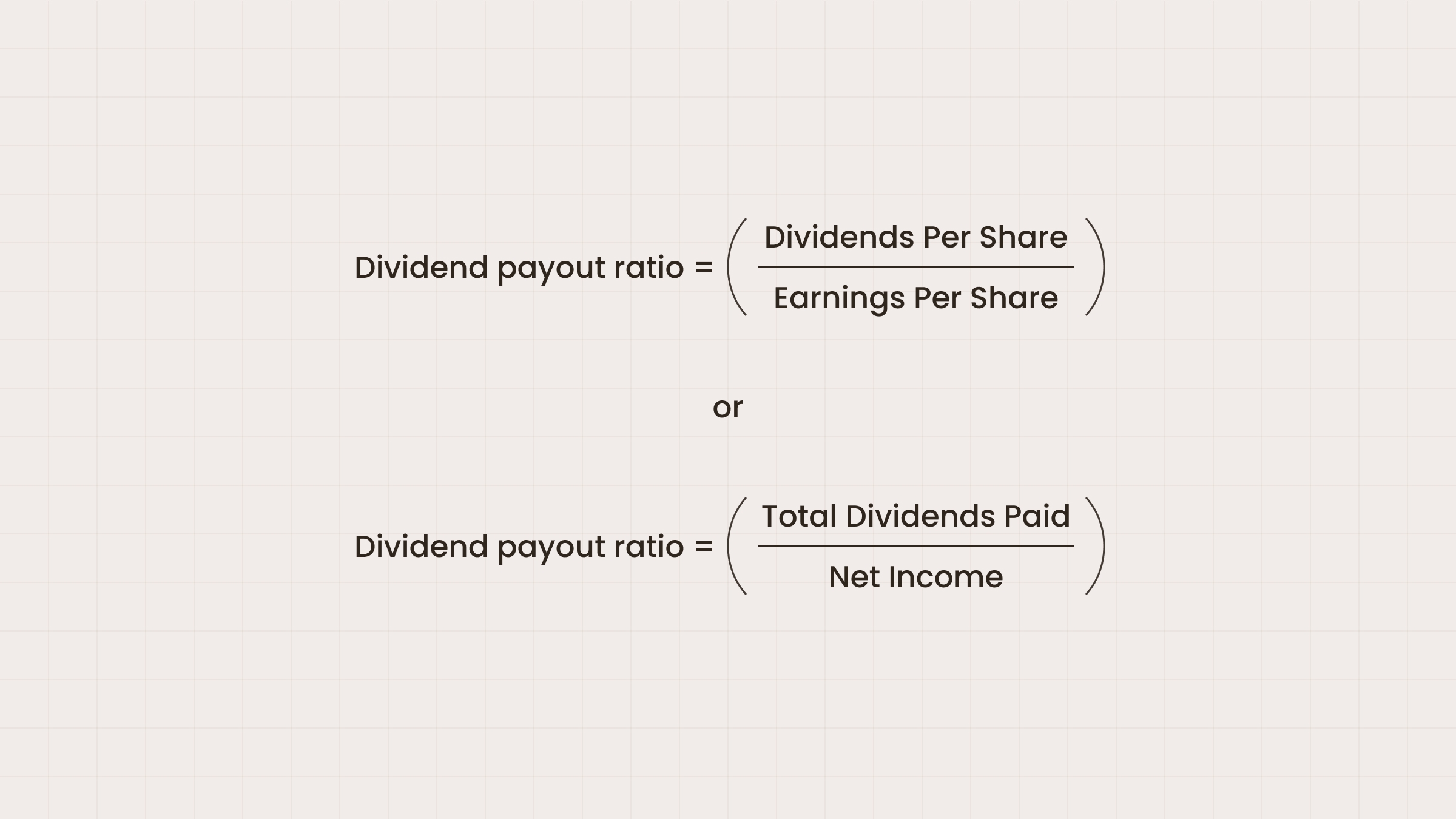

What is a payout ratio?

The payout ratio is a metric used to assess the proportion of a company's earnings that is distributed to shareholders as dividends. It is calculated by dividing the total annual dividends paid by the company by its net income.

The formula for the payout ratio is:

The payout ratio is expressed as a percentage. For example, a payout ratio of 40% means that the company pays out 40% of its earnings in the form of dividends, while retaining 60% for reinvestment or other purposes.

This metric helps investors evaluate a company's dividend sustainability. A low payout ratio may indicate that a company has room to increase dividends, while a high payout ratio could suggest that the company is distributing a large portion of its earnings, which may not be sustainable in the long term. Investors often use the payout ratio to compare companies within the same industry and assess the attractiveness of dividend-paying stocks.

What is a balance sheet?

A balance sheet is a financial statement that provides a snapshot of a company’s financial position at a specific point in time, detailing its assets, liabilities, and shareholders' equity. In relation to dividends, several aspects of the balance sheet are particularly relevant:

1. Retained earnings: This is part of shareholders' equity and represents the cumulative profits that a company has retained after paying out dividends. When dividends are declared and paid, retained earnings decrease, reflecting the distribution of profits to shareholders.

2. Dividends payable: When a company declares a dividend but hasn't yet paid it, the amount appears as a current liability on the balance sheet under "Dividends Payable." This indicates the company’s obligation to pay those dividends to shareholders and is recorded until the payment is made.

3. Shareholders’ equity: The balance sheet shows the total equity available to shareholders, which includes issued share capital plus retained earnings and any other equity components. When dividends are paid out, the retained earnings part of equity is reduced, impacting the overall shareholders' equity.

In summary, the balance sheet reflects the implications of dividend payments on a company's financial health and profitability, highlighting how much profit is distributed to shareholders versus retained for reinvestment in the business.

What are dividend dates?

Dividend dates refer to specific dates that are important in the process of paying dividends to shareholders. These are the key dividend dates:

Declaration date

This is the date when a company's board of directors announces the intention to pay a dividend. The announcement includes details about the amount of the dividend and the associated dates.

Ex-dividend date

This is the cutoff date for determining which shareholders are eligible to receive the declared dividend. If an investor purchases shares on or after this date, they will not receive the upcoming dividend. The ex-dividend date is typically set one business day before the record date.

Record date

This is the date when the company checks its records to determine which shareholders are entitled to receive the declared dividend. Shareholders must be on record as owning the shares by this date to receive the dividend.

Payment date

This is the date when the dividend is actually paid out to shareholders. On this date, funds are either transferred electronically or checks are mailed to eligible shareholders.

Understanding these dates is crucial for investors who want to capitalize on dividend payments and plan their investments accordingly.

The first public company recorded to have paid regular dividends was the Dutch East India Company from 1602 to 1800.

How dividends affect stock price

Dividends can significantly impact stock prices in several ways:

Investor perception | When a company announces or increases its dividend, it often signals financial strength and stability, which can boost investor confidence. This positive perception may lead to increased demand for the stock, driving up its price. |

Income attraction | Dividend-paying stocks are attractive to income-focused investors, such as retirees. Increased demand from these investors can put upward pressure on the stock price, especially for companies known for reliable dividend payments. |

Value adjustment | On the ex-dividend date—the day after the record date—stock prices typically adjust downward to reflect the payout of the dividend. This drop occurs because the value of the dividend is no longer part of the company’s assets. For example, if a company pays a $1 dividend, the stock price might decrease by approximately $1 on the ex-dividend date. |

Market conditions | Broader market trends can influence how dividends impact stock prices. In a bull market, the effect of dividends on stock prices might be muted by overall investor optimism. Conversely, in a bear market, a strong dividend might provide a cushion for the stock price, as investors seek safety in reliable income. |

Payout ratio and growth expectations | A high payout ratio may signal limited growth potential, which could negatively affect the stock price if investors believe the company is prioritizing dividends over reinvestment in growth opportunities. Conversely, companies with a balanced approach to dividends and growth can attract a broader base of investors. |

Overall, while dividends can affect stock prices immediately—especially around ex-dividend dates—the long-term effects depend on a company's overall performance, growth prospects, and market conditions.

Qualified vs. non-qualified dividends

Qualified and non-qualified dividends refer to the tax treatment of dividend payments at the federal level in the United States.

Qualified Dividends

Definition:

Qualified dividends are dividends paid by U.S. corporations or qualified foreign corporations on stocks that have been held for a certain period.

Tax rate

They are taxed at the long-term capital gains tax rates, which are generally lower than ordinary income tax rates. For most taxpayers, this ranges from 0% to 20%, depending on their taxable income.

Holding period

To be considered qualified, the stock must typically be held for at least 61 days during the 121-day period that begins 60 days before the ex-dividend date.

Non-Qualified Dividends

Definition

Non-qualified dividends, also known as ordinary dividends, are dividends that do not meet the criteria for qualified dividends.

Tax rate

They are taxed at ordinary income tax rates, which can range from 10% to 37%, depending on the taxpayer's income level.

Characteristics

These include dividends from sources like real estate investment trusts (REITs), master limited partnerships (MLPs), or dividends on stocks held for a shorter period than the required holding period.

Understanding the distinction between qualified and non-qualified dividends is essential for tax planning and optimizing investment returns.

What entities pay dividends

Dividends are typically paid out by various types of entities, primarily corporations, but they can also include other organizations. Here are the main types of entities that pay dividends:

Publicly Traded Corporations

These are the most common entities that pay dividends. Established companies in sectors such as utilities, consumer goods, and financial services often distribute a portion of their profits to shareholders as dividends.

Real Estate Investment Trusts (REITs)

These entities invest in income-producing real estate and are required by law to distribute at least 90% of their taxable income to shareholders in the form of dividends, making them attractive to income-focused investors.

Master Limited Partnerships (MLPs)

Similar to REITs, MLPs provide dividends, often referred to as distributions. They primarily operate in the energy sector and are required to distribute a significant portion of their earnings to unit holders.

Mutual Funds and Exchange-Traded Funds (ETFs)

Some funds that invest in dividend-paying stocks will pass on the dividends received from their holdings to investors as dividend distributions.

Private Companies

While less common, some private companies may pay dividends to their shareholders, particularly if they have consistent profits and a strategy focused on returning value to investors.

Banks

Many banks periodically pay dividends to their shareholders, reflecting their profitability and stability.

These entities vary in how they determine their dividend policies, but they all aim to provide returns to their investors.

Summary

Dividends are payments made by a company to its shareholders, typically derived from profits. They can be issued as cash or additional shares and are often expressed as a fixed amount per share or a percentage of the share price. Dividends provide a source of income for investors and signal a company's financial stability. The decision to pay dividends and the frequency of payments depend on a company's earnings, cash flow, and dividend policy. While dividends can enhance shareholder value, they are not guaranteed and can be adjusted or suspended based on the company’s financial condition.